Creators of the Future

Coming up with goods or services that nobody else on the market can offer is what makes a breakthrough technology and determines the future. But is this sort of future meant for the BRICS countries? Vladimir Korovkin, author of the BRICS Innovations Stars report, is confident that it does, and to prove his point, he cites examples of the most accomplished companies in the BRICS countries. They are all privately owned, successful on the global and domestic markets, and promote innovation.

The idea of innovation is quite new. Even half a century ago, the majority of the world’s population – even in the so-called ‘developed countries’ – focused on perfecting existing methods and approaches, and placed little value on change. There was even an old Chinese curse that said, “May you live in changing times.” It would appear as though we are all thoroughly cursed – we now live in a time of turbulent changes. However, adapting to these changes is the key to success. This holds true on a personal level, in corporate development, and in national policy.

BRICS countries are responsible for a significant and growing portion of the world’s economic development. But until recently, most people associated these countries with supplying natural resources and cheap labor to the global market, and they supposedly lagged behind in the innovative sectors of the global economy.

There is growing recognition of the huge leap that BRICS companies have made in the last decade. Many of them have reached leading global positions for products and services traditionally dominated by ‘developed’ economies, such as computer equipment and software, high-precision industrial equipment, new material development, etc. This success is more and more often achieved through factors other than price competitiveness derived from a lower cost base.

BRICS innovations are likely to become a formative trend of the global economy in the 21st century. They have the potential to re-establish trade routes and re-define the notions of cultural similarities and differences with a corresponding influence on the issues of power and politics. Still, there is limited research and literature on this topic.

We set out to study BRICS innovations on two levels, macro and micro, and tried to paint a holistic picture of the trends we noted and also understand the driving force behind these innovations – the companies. For the macro view, we rely on meta-analysis of available research projects with a focus on corresponding authoritative indexes. For the micro level, we looked at the case studies of BRICS companies that have made innovations their lifeblood to achieve commercial success not only on the national level, but also in the global arena. Through those case studies, we explored and discovered the underlying tools of innovative companies in emerging markets.

The outcome of both components of our research should inspire managers to develop their corporate expansion strategies, and also to help policymakers create institutions and environments that will boost the innovative capabilities of the BRICS countries (and others).

BRICS countries: Innovations measured and compared

Singapore, Hong Kong, and South Korea provide a more holistic picture of innovation metrics. Each country has substantial strengths. Singapore is first in business sophistication, human capital, and infrastructure, and is fourth in market sophistication. Hong Kong leads the world in infrastructure and is third in market sophistication. South Korea is third in human capital, fifth in infrastructure and sixth in knowledge and technology output

The idea of innovation is quite new. Even half a century ago, the majority of the world’s population – even in the so-called ‘developed countries’ – focused on perfecting existing methods and approaches, and placed little value on change. There was even an old Chinese curse that said, “May you live in changing times.” It would appear as though we are all thoroughly cursed – we now live in a time of turbulent changes. However, adapting to these changes is the key to success. This holds true on a personal level, in corporate development, and in national policy

The annual Global Innovation Index (which we will refer to hereafter as ‘GII’) was developed jointly by the Johnson Graduate School of Management at Cornell University, INSEAD, and WIPO (World Intellectual Property Organization), and is the key international source for comparing different countries’ innovation capabilities and results. The index combines over 80 metrics seeking to measure both ‘input,’ which describes a country’s potential, and ‘output,’ which is the end result of that potential. Their relationship is the measure of a country’s innovation efficiency. It is important to note that ratings like this – unlike credit ratings, which imply direct consequences – are constructed in an attempt to reflect reality. However, we believe that they are great tools for practical lessons when comparing the strengths and weaknesses of the BRICS economies as related to each other and the ‘outer world.’ This analysis can be instrumental in formulating approaches to solve the key issues of macro innovation management, which seems to be the best operating mode within the complex set of relationships between state-level measures and actions, and between the initiatives of private companies and entrepreneurs.

The annual Global Innovation Index (which we will refer to hereafter as ‘GII’) was developed jointly by the Johnson Graduate School of Management at Cornell University, INSEAD, and WIPO (World Intellectual Property Organization), and is the key international source for comparing different countries’ innovation capabilities and results. The index combines over 80 metrics seeking to measure both ‘input,’ which describes a country’s potential, and ‘output,’ which is the end result of that potential. Their relationship is the measure of a country’s innovation efficiency. It is important to note that ratings like this – unlike credit ratings, which imply direct consequences – are constructed in an attempt to reflect reality. However, we believe that they are great tools for practical lessons when comparing the strengths and weaknesses of the BRICS economies as related to each other and the ‘outer world.’ This analysis can be instrumental in formulating approaches to solve the key issues of macro innovation management, which seems to be the best operating mode within the complex set of relationships between state-level measures and actions, and between the initiatives of private companies and entrepreneurs.

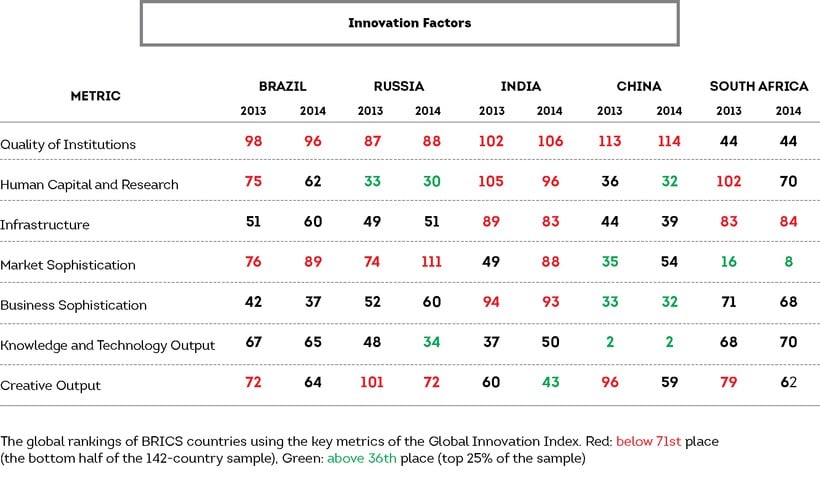

The 2014 BRICS economies have a wide dispersion of ratings and do not cluster around one set of scores. While China is ranked 29th and Russia has entered the global top 50 for the first time (at 49), South Africa ranks 53rd, followed by Brazil in 61st and India in 76th place. Four of these countries have made considerable progress over the last year; in 2013 China was ranked 35th, South Africa was 58th, Russia was 62nd, and Brazil was 64th. Regrettably, India fell 10 places, and is now in 66th place. The picture is somewhat different using the ‘efficiency’ measure. China was among the world’s top performers in 2014 in 2nd place (a leap from an already respectable 14th place in 2013), India was 31st (but with a sharp decline from 11th in 2013), Russia was 49th (another impressive leap, from 104th), Brazil was 71st (slipping a bit from 69th), and South Africa, while improving by six positions, was still in 93rd place. These statistics are directly related to policy issues. It would be quite understandable if BRICS countries were largely in the middle of world rankings due to innovation problems, institutes, and infrastructure, but it looks like with the exception of China they are not succeeding in getting enough output from the resources they have. This hypothesis requires more examination, but if proven true would require serious action.

Part of this lack of efficiency may come from a lack of overall balance in innovation development. A pattern emerges if we look at specific Index metrics. That is, every country has its strengths, and are even world leaders in certain regards. China ranks second in the world in ‘technology output’ and is a leader in ‘education,’ India is first in ‘communications, computer, and information exports’ (a sub-metric of ‘technology output’), South Africa leads the world in ease of obtaining credit (and is in the top 10 in overall ‘market sophistication’), Russia is traditionally strong in tertiary education (an important factor in ‘infrastructure’) and also in domestic patent and utility model applications (‘technology output’), and Brazil is strong in ‘knowledge absorption’ (‘business sophistication’) as measured by royalty and license fee payments, high-tech imports, or computer and information service imports.

Nevertheless, the BRICS countries fall below global averages in many other areas, making for an uneven overall picture. It is this imbalance that clearly distinguishes the current state of innovations in BRICS markets from the more innovative countries.

Possible role models

To set clear goals and develop roadmaps to reach them, it is useful to look beyond the BRICS countries for models of quick innovation (not discounting China’s progress as one of the global leaders in technological output). Three of the top 20 countries stand out in this respect: Singapore (7th), Hong Kong (10th), and South Korea (16th). Much has been written in business and academic literature about these countries’ path to innovation leadership, and there seems to be wide consensus by the BRICS countries that this success can be replicated more effectively than the paths of other top performers, such as the countries of Western Europe or the United States.

Singapore, Hong Kong, and South Korea provide a more holistic picture of innovation metrics. Each country has substantial strengths:

- Singapore is first in business sophistication, human capital, and infrastructure, and is fourth in market sophistication.

- Hong Kong leads the world in infrastructure and is third in market sophistication.

- South Korea is third in human capital, fifth in infrastructure and sixth in knowledge and technology output.

More importantly, none of these countries have substantial weaknesses. They are in the top 25% of virtually all aspects of innovation. It would not be an overstatement to say that these possible role models have created fully balanced systems, resulting in synergy between all the institutions and actors involved. This wide-reaching approach is what the BRICS countries currently lack and what they should adapt to develop their innovativeness.

Сountry and company strategies

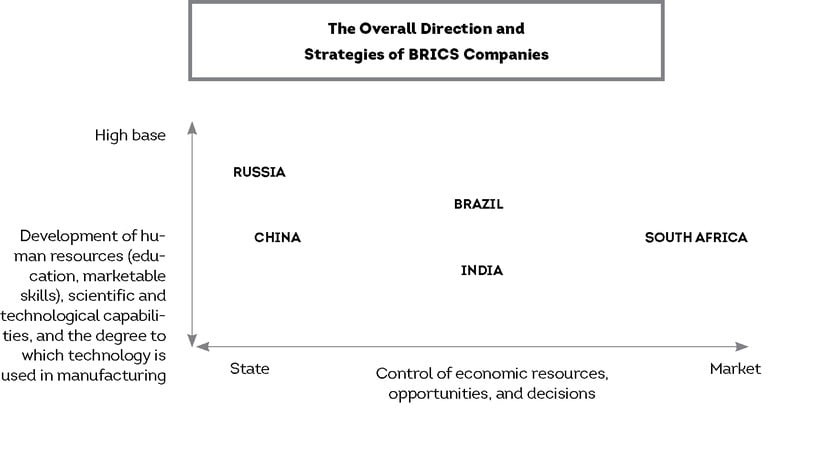

If we jump back to the BRICS countries to further study their ‘innovation’ profiles, it would be impossible to ignore the differences in their economic and social history. These variances force companies to develop different approaches to market success, though the underlying pattern is the same: to find an area of relative strength in the country’s environment and to determine a way to make it productive domestically and globally. The differences in environments can be evaluated along two axes: ‘market control vs. state control’ and ‘high base vs. low base,’ using the time period of the 1990s (not taking into account complex cycles of economic development on the long historic horizon).

This map shows the overall direction and strategies of BRICS companies:

Russia could take advantage of a relatively high technology and human development base, but has to overcome the ingrained patterns of a state-run economy to build business models that are internationally competitive.

China was starting from a relatively low technology base and lacked a skilled labor force, but it was this deficiency that allowed for rapid improvement. Chinese companies had room to learn and did not have to waste their energy overcoming existing systems – their imperfections and inadequacies were fully recognized on the state level.

India and Brazil shared a tradition of mixed economic environments. They both had a largely free market for small and medium businesses, and big corporations faced considerable intervention from the state, including protectionism on the domestic market. Of the two, Brazil tended to have a higher technology and human development base, and both countries thought it essential to bring more private initiative and competition into the corporate sector. Yet in human development, India had the advantage of a largely English-speaking population, which permitted the country to quickly integrate its vast labor force into the global market. The two countries also have large agricultural resources and rural populations in common, and both had some innovative strategies that capitalized on this.

South Africa came from a rather liberal market environment, but had a striking divide in human capital between its different social groups (this problem is also relevant to India, where affirmative action on the constitutional level has been necessary to overcome the legacy of the caste system). Its overall technology and human development base was low, but there were groups with development levels that were high compared to the rest of the continent. As a result, the country enjoyed the position of being the undisputed leader of one of Sub-Saharan Africa’s large and resource-rich regions – albeit a turbulent one. Many of South Africa’s business strategies were successful because they were able to take advantage of this opportunity.

Case studies of BRICS companies confirm and build upon these findings. The Russian companies which achieved international prominence, or even dominance, through innovation share remarkably similar histories. A typical Russian ‘high-tech star’ is not at all a product of the internet era – even companies like Yandex, ABBYY, or Kaspersky, which are globally recognized for their online services, actually date back to the early 1990s. Those were the formative years, when the scientific advances of Soviet schools met with the enthusiasm of the first Russian entrepreneurs. The high level of Soviet science and technology, combined with a strong educational infrastructure, was strong enough to overcome the deficiencies in the market and business institutes. This resulted in strong technological output, as demonstrated by the cases of Infowatch, Speech Pro, Diakont, and Skif-M. These companies all managed to obtain a significant export share of high-tech products in fields where the USSR was a global pioneer, such as laser systems, fiber optics, and cryotechnology, and also in the development of software that was booming in the early 1990s. The same concentration of innovative industrial efforts can also be observed among state-controlled actors (large corporations and research institutes) that were beyond the scope of our study. However, it is likely this focus that prevents the large state-run corporations – operating in natural resources like oil and gas, and essentially multi-national players – from becoming important global innovators.

The Russian innovation champions are about to celebrate their silver jubilee, or the 25th anniversary of their launch. They are privately owned and operated (though sometimes with institutional shareholding from specialized funds), have a host of international patents and awards, and boast sales ranging from $30 million to $300 million. There are a few exceptions to this rule – the public company IPG Photonics is now headquartered in the US and has sales over $700 million, and Yandex has sales topping $1.5 billion – but most of the companies that met our research criteria prosper as solid medium businesses

Chinese companies initially had little more to rely on than the industriousness of their people. In theory, they had every strategic opportunity for industrial development. But to build up their industrial base they had to find the money to acquire the necessary modern technology. However, they had the sheer size of the potential market on their side, even though the market had to be created out of tightly administrated distribution systems for that potential to be realized. This dilemma was solved with ‘technology in exchange for labor and market access’ deals. The bargain proved to be beneficial for Chinese companies; they gradually became tech-empowered suppliers to the domestic market, and eventually made many technical breakthroughs as well. Lenovo and Huawei are the most high-profile cases, and there are much more in different market segments. Nowadays, China is among the global leaders in R&D investment and patent applications, which is reflected in its ‘technology output’ standing. Considerable challenges lies ahead, however. Observers note that ‘creative output’ will not be that easy to crack; many cultural traditions serve as barriers against ‘disruption’ and ‘disregard for authority,’ which are often seen as the foundation of modern creativity.

India and Brazil managed to create a narrow but strong group of ‘national champions,’ who combine cost and innovation in their competitive propositions. This is not an easy feat, but the cases of companies like Wipro and Braskem show that both countries are prepared to meet the challenge. While the general level of human development in these countries is below the OECD level, they have managed to create and exploit ‘advanced megacities,’ like São Paulo or Mumbai, which have attracted some of the most innovative businesses in the world. As mentioned above, Indian companies were able to take advantage of the abundance of low-cost, middle-skilled English-speaking workforce to step up as providers of all types of outsourcing services. Brazil’s contribution to the world economy likely lies in innovative approaches to agriculture, reinforced by the recent global movement for ‘greener’ technologies.

South Africa was effective in capitalizing on its strong market environment to nurture the global e-commerce mega-player Naspers, now worth almost $50 billion, and in making investments all over the world, including substantial holdings in BRICS markets (like Russia’s Mail Group, Slando, and Avito). Strategies also arose from the country’s unique position in Africa. Dimension Data is but one example – it managed to position itself as a gateway between Sub-Saharan Africa and the modern IT world.

Russian innovation champions

Let’s go back to the ‘collective biography’ of the Russian innovation champions, who are about to celebrate their silver jubilee, or the 25th anniversary of their launch. They are privately owned and operated (though sometimes with institutional shareholding from specialized funds), have a host of international patents and awards, and boast sales ranging from $30 million to $300 million. There are a few exceptions to this rule – the public company IPG Photonics is now headquartered in the US and has sales over $700 million, and Yandex has sales topping $1.5 billion – but most of the companies that met our research criteria (truly innovative, private, successful globally or dominant on the domestic market) prosper as solid medium businesses. Another remarkable quality is the narrow technological field where our champions are concentrated; they did not usually extend beyond the strongholds of Soviet science.

At the moment, it is important to learn how to increase private innovation in Russia and how to help existing mid-size innovators grow bigger. They would be privy to a whole host of new opportunities if they could leap into the $1 billion sales range, but they are still quite far from that target. To make this leap, they need to simultaneously expand their breadth and depth by increasing their global market niches, expanding into related fields, and becoming full-service suppliers. Both of these goals could be achieved through M&A in countries where there is enough ‘market sophistication,’ but Russia lacks non-organic growth opportunities. The 1990s and early 2000s were bad years to launch new companies in Russia (aside from those in e-commerce), so there is currently a vacuum of possible acquisition targets in the local market. Screening for possible acquisition targets abroad requires a whole different set of management skills and a sufficiently higher level of financial capabilities. The cost of credit in Russia is also close to being prohibitive for financing bold deals, but without those deals a company is likely to meet a glass ceiling before it can grow into a big business. This is an important problem, which gets surprisingly little attention in the Russian business world. Still, the timeframe may be limited – in a decade or so, the founders of the ‘innovation champions’ may start to think about retirement, and then their companies are likely to go to the target side of the M&A market.

The key finding from our research is that Russia differs from the emerging markets in its innovation development trajectory, in that it has trouble bringing innovation down to relatively simple, yet mass produced, things. However, the recent success of local internet companies indicates that this barrier can be overcome. In the modern world, there is little difference between producing an effective digital user interface and an equally effective physical product. If Yandex can defend its domestic market from Google by creating a number of world-class products, there is no reason why a Russian car company could not do the same in its market.

It is crucial to get Russian innovators to think big and get out of the comfort zone of market niches. They may need some macro support and encouragement, but that will not completely eliminate market risks and challenges. It is through stubborn competition where it pays, not where it is easy, that innovative economies have been built. As for country-level policy making, it has an important role in creating the institutions and infrastructures that are conducive to innovation and economic success.

BRICS: an innovative future

BRICS countries have made impressive progress in the world of innovation. There are many statistics that support this, but personal stories may better illustrate this point. Back in 2004, none of the BRICS countries were home to global innovators. But now we are no longer surprised to see companies from Brazil, China, Russia, India, or South Africa at the top of global ratings.

China was starting from a relatively low technology base and lacked a skilled labor force, but it was this deficiency that allowed for rapid improvement. Chinese companies had room to learn and did not have to waste their energy overcoming existing systems – their imperfections and inadequacies were fully recognized on the state level.

The bargain proved to be beneficial for Chinese companies; they gradually became tech-empowered suppliers to the domestic market, and eventually made many technical breakthroughs as well

It is important to observe and analyze the challenges and shortcomings of innovative developments in the BRICS countries, both on the macro and micro level. Measures could be taken to maximize current input, and there is still more potential in expanding the innovation development base. Human development is the key issue – there needs to be a focus on increasing the general education level as well as improving technical and business creativity in the global arena. Here, the BRICS countries can strengthen their futures by joining together in economic and humanitarian cooperation and sharing their remarkable diversity of resources.

Sector: Auto

Sector: Auto

Revenues: $32 billion

Assets: $28 billion

Employees: 66,000

Ticker: TTM (US)The Company

Tata Motors Limited manufactures and sells commercial and passenger vehicles, primarily in India but increasingly around the world. After starting with mostly heavy commercial vehicles, the company’s product mix has evolved over the last 50 years to include utility vehicles and midsize, small, and compact passenger vehicles. The company also makes and sells vans, trucks, buses, and all-terrain vehicles. More recently, the company has expanded its offering to luxury and sports cars and even defense vehicles. At the forefront of innovation, the company has been experimenting with electric and fuel cell vehicles. Upstream, the company has captured a growing market in vehicle components – providing engineering, design services, machine tools, and factory automation services to other auto companies. Downstream, the company has expanded its offerings through its own dealerships, sales and service forces, finance and spare parts branches, and affiliates in Southeast and South Asia, Africa, the Middle East, South America, the Former Soviet Union, and Europe. The company is based in Mumbai (India) with production facilities in Lucknow, Dharwad, Jamshedpur, Pantnagar, Sanand, and Pune, as well as in Argentina, South Africa, Thailand, and the UK.

The Innovation(s)

Methodology of the Case Studies

GENERAL APPROACH

- Approach structured on the ‘Oslo Manual’ by OECD

- Focused on innovations in products and processes (production and delivery)

RESEARCH SAMPLE

- Privately or publicly (non-state) owned companies

- Focused on innovations (no a priori industry filter)

- Companies that achieved global market success through their focus on innovations

DATA COLLECTION

- Performed by an international team of researchers with significant contributions from Professor Bryane Michael (Hong Kong University), Alexey Andreev (Russian Foreign Trade Academy), and Alexander Svetlov (Dentsu-Smart, Advertising Agency)

- Overall, over 1,200 companies were sampled and more than 40 were studied extensively

The Nano brings cars to the masses. The car’s retail price of $1,700 represents one of the lowest prices for a passenger vehicle anywhere. Its price comes in at slightly more than the annual salary of the average Indian – explaining average yearly sales of about 60,000 units since its introduction in 2009. The car benefits from new design and technology techniques (embodying over 30 design patents and almost 40 process and product patents).

Three things make the Nano – and Tata Motors by extension – radically innovative. First, the design reflects blank-slate re-engineering proposed by management gurus like MIT professor Michael Hammer. The car rethinks automotive design (from making the truck accessible only from the inside to three lug-nuts on the wheels rather than the traditional four). The designers clearly accepted nothing from the usual design tenets with this car. Second, using what academics and management gurus call ‘modularized sourcing,’ the car represents the assembly of parts and modules made by others. Suppliers from Bosch to ZF Friedrichshafen produce and supply almost everything the car uses. Third, and as a consequence of the first two points, the Nano’s price comes in at 5-10% of typical cars in the developed world. Such pricing threatens, and promises, to have the same effect on the motor industry that RyanAir had on the airline industry.

The Future

Tata has plans to sell the Nano in markets like the US. If the Nano captures even 1% of the US automotive market in 2016, the company would sell 150,000 units. The US already represents India’s largest export market for cars – a trend the Nano would certainly accelerate (if it could). Tata also has plans to make electric power train and fuel cell versions. The company’s dedication to innovation is beyond doubt – it uses its own ‘Innometer’ to measure innovative output aimed at achieving domestic and global sales and other benchmarks.

Yet Tata’s (and the Nano’s) success remains far from guaranteed. Suzuki’s (Maruti Suzuki in India) Maruti Alto 800 still represents one of India’s most popular cars – with sales far ahead of the Nano despite its 50% higher price. Moreover, the car deliberately seeks to go head-to-head with India’s booming, entrenched, and cheap two-wheel (scooter and motorcycle) industry. Both Bloomberg and Businessweek report that the Nano has “flopped” and “sputtered” respectively. Car fires and safety issues have also plagued the upstart car. Will management scholars look back and see the Tata as the next Ford or Toyota? A couple of year’s sales should tell…

Sector: Petrochem

Sector: Petrochem

Revenues: $18 billion

Assets: $20 billion

Employees: 8,000

Ticker: BAK (US)

The Company

Braskem represents Latin America’s largest petrochemical maker, and a leading chemical maker worldwide. The company produces complicated-sounding things like ethylene, propylene, polyethylene, and so forth. At the risk of over-simplifying the company – it works in five major segments. Its basic petrochemicals segment deals in a range of fuels, it has a plastics segment, a vinyls segment, a chemical distribution segment which deals largely in solvents, and a general purpose chemicals segment, dealing with a range of specialty chemicals (like pharmaceuticals). The company also trades in utilities like water and gas as well as provides industrial services. Traditionally (until the last 10-20 years), Braskem has represented just another petrochemical maker. Yet a range of innovations have separated this company from the petrochemical pack.

The Innovation(s)

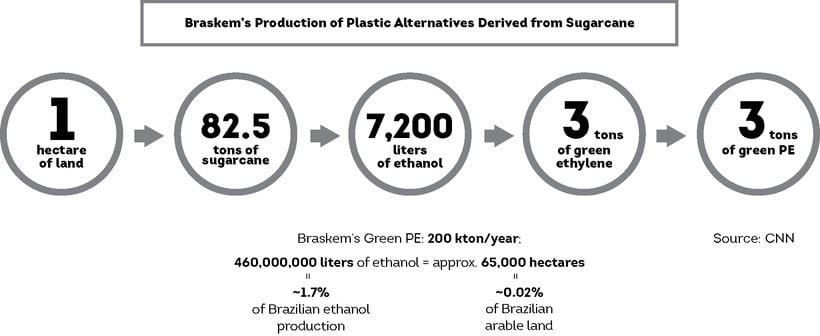

The plastics you see in the room around you come from barrels and barrels of crude oil. The plastic bits covering your computer, much of your chair’s body, and even structural components in the building you are sitting in come from ‘cracking’ oil. Breaking down oil into plastics results in atmosphere-polluting carbon dioxide and usurps scarce oil supplies from other uses (like air and car travel). What if we could make oil from plants instead of fossil fuels? Plants remove CO2 from the atmosphere and the products could be recycled as easily as their petroleum-based counterparts. Braskem has invented such a process. As shown in the figure above, Braskem’s process uses sugarcane – rather than fossil fuels – as the input in the plastics-making process. The company produces about 0.25% of the world’s 80 million tons of plastics.

Braskem’s process represents a groundbreaking innovation for three reasons. First, the sugar-cane plastics industry represents the perfect example of Professor Anita McGahan’s ‘radical industry change.’ Braskem has found a new and better input into a $700 billion worldwide industry. The processing machines used to turn ethanol into ethylene do not even need modification to handle sugar cane-sourced ethanol. Second, Braskem’s process represents social (as much as economic) entrepreneurship. Braskem capitalized on increasing environmental awareness to find an input that actually reduces greenhouse gases. By tackling a social issue and an economic issue simultaneously, the company could likely ask for a price premium. Governments will like the lower negative externalities associated with a non-petrol plastics production process. Consumers will like the lower prices (oil is far more scarce in the long run than sugarcane). Third, if other parts of the oil refining and production industry open to radical innovation from using sugar cane, Braskem’s patents could find their way into a number of other uses. Imagine if sugarcane served our energy production, chemical production, and travel needs in the future. Robert Cantrell has argued that competition between companies in the future will consist of competition between patents. As Braskem jumps on an important new industry, its patents and un-patentable organizational skills will redefine at least one industry: plastics.

The Future

If Braskem’s future looks like its past, it will likely be called Worldkem in the future. Acquisitions made around 2010 have already made Braskem a leading polypropylene producer in the US and given the company a presence in Europe (headquartered in Germany). The company’s acquisition of Quattor (Brazil’s second largest petrochemical company) has made the company the world’s eighth largest petrochemical company. But despite its important advances in sugarcane plastics, ethanol still represents only 5% of the company’s raw materials. Braskem is still an oil company – and not even one of the world’s top 10 (yet!). Can Braskem stand toe-to-toe with giants like Germany’s BASF, the US’s Dow Chemical, China’s Sinopec, or the UK’s Ineos Group? These companies’ sales of almost $200 billion dwarf Braskem’s – as do their patent profiles. Will sugarcane help Braskem break into the global petrochem giants?

Sector: IT

Sector: IT

Revenues: $7 billion

Assets: $8 billion

Employees: 146,000

Ticker: WIT (US)

The Company

Wipro represents one of India’s best-known success stories. Based in Bangalore, the company weighs in as the world’s 7th largest information technology (IT) services firm. The company operates two main segments – IT services and products. Its IT services segment offers a wide-range of business process outsourcing and other solutions. Some of these include software application development and maintenance services, research and development services for hardware and software design, and business analytics and intelligence. The company’s consulting services include product engineering, enterprise-wide applications, and cloud services. Some of its clients come from financial services (including banking and insurance), healthcare, retail, industrial, energy, media and telecom, and the list goes on. The company sells its own branded desktop computers, servers, and notebooks. The company has made a major push in recent years to become a green computer company – minimizing its environmental footprint.

The Innovation(s)

Each day, Wipro’s employees invent millions of solutions to companies’ IT challenges worldwide. They also perform other ‘back office’ operations, which solve problems for millions more customers. Collectively, these daily innovations add up to one of the most important innovations in international business in the late 20th century – business process outsourcing. British Airways, General Electric, and American Express represent only some of the better-known companies using Indian-centered business process outsourcing. The sector comprises roughly 1% of Indian GDP – and is a model many other emerging markets have longed to copy. Wipro started it all.

Wipro’s

model represents a unique innovation for three reasons. First, Wipro

represents the first major case of ‘flexible standardization.’ Many

management gurus have written about Toyota’s ‘flexible specialization,’

the company’s ability to change its standardized assembly lines to fit

custom orders. No one has written about Wipro’s converse business model –

its ability to take highly specific tasks and standardize them

thousands of miles from where the service is being delivered. Second,

Wipro flies in the face of almost 40 years of organizational theory.

Management theorists like Chandler and Williamson told us that companies

should develop specialized IT functions as they grow. Companies will

find it cheaper and more reliable to make their software and run their

own enterprise applications. Only a super-cost competitive service could

disrupt the logic of corporate IT internalization. Wipro has seemed to

defy the experts, providing prices that make IT outsourcing cheaper than

doing it in-house. Third, its multi-line focus (from computers to

services) has created a business cluster in its Bangalore hometown.

Wipro had helped create an innovation cluster long before management

gurus like Porter and Florida started writing about Silicon Valley and

its rivals. The company’s 146,000 strong staff does everything, from

making computers to engaging in business process outsourcing. Wipro’s

size stamps such a large footprint in Bangalore that the company has

attracted talent and fostered the creation of a local cluster. The

creation of Bangalore’s IT cluster in many ways owes its existence to

Wipro. And Wipro continues to benefit from the cluster it helped create.

We’d say Wipro’s innovation consists of innovating innovation.

The Future

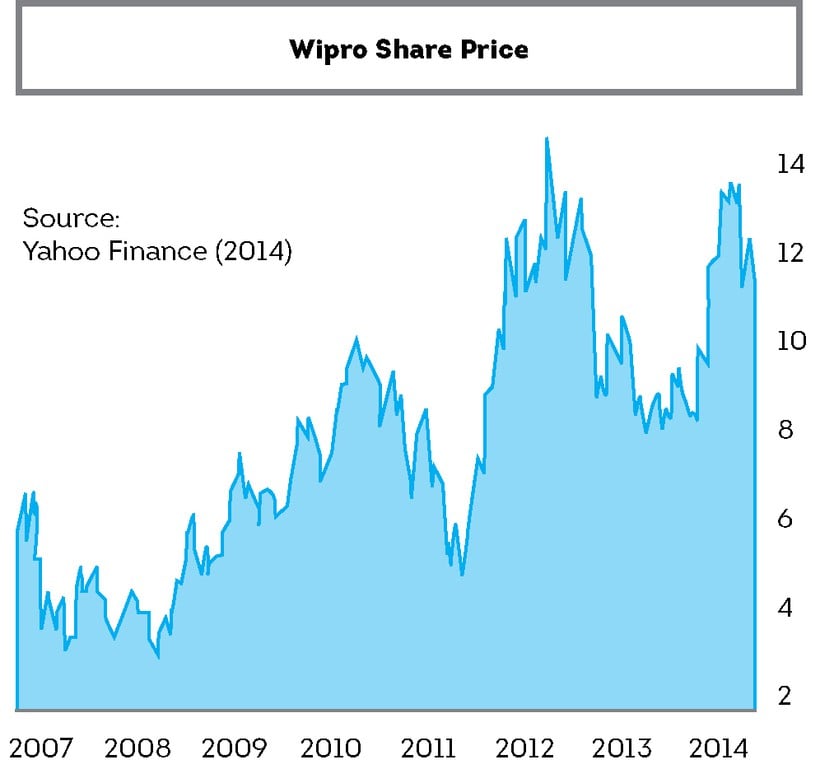

Wipro looks likely to tread water into the foreseeable future – existing in an industry where innovation has become banal. The company’s share price has just about doubled since 2005. Yet competitors like Infosys and their US rival Cognizant have made inroads into the industry Wipro helped create. Wipro’s recent spin-off of its non-core businesses make the company less diversified – and more focused. Wipro’s recent innovations have focused on getting companies ready for the Internet of Things and Everything Digital revolutions. If Wipro can capture global mindshare in these spaces as effectively as in outsourcing, the company could shine again.

Sector: IT

Sector: IT

Revenue: $6 billion

Assets: N/A

Employees: 23,000

Ticker: NTT (parent since 2010)The Company

Dimension Data represents one of South Africa’s IT success stories. Dimension Data focuses on its service offerings more than its products. Its revenue comes mainly from systems integration (77%), requiring an extensive understanding of the relationships between its users and its data. In theory, product revenue came in at 59% of the company’s 2012 revenue. However, such a ‘product’ consists of software and IT as a service-based solution. Managed services come to 28% of revenue and professional services are 13% of the firm’s revenue. Relationships become particularly important in software as a service (SaaS) model. In such a scheme, the user only pays for services they use – encouraging the company to be as ‘sticky’ as possible.

Founded in 1983 as an information technology (IT) company, Dimension Data was listed on the Johannesburg Stock Exchange just four years later. In the early 1990s, the company became a Cisco Gold Partner – starting a relationship that endures to this day. The company also expanded into software and service-provision in Sub-Saharan Africa. The company’s 2000 listing on the London Stock Exchange echoed the push into the North American, European, and Asian markets. By launching its globally standardized managed-services offerings (its proprietary Global Services Operating Architecture) the company helped solidify its service orientation – by providing clients with 24/7 remote network monitoring and maintenance services.

Throughout the 2000s, the company grew quickly both organically and through acquisitions, in cloud computing in particular. The company bought OpSource Inc. and BlueFire, rebranded them as Dimension Data companies and introduced its new Cloud Solutions Business Unit, and became one of the strongest global players in the segment. This was recognized by Gartner, which positioned the company in the ‘Leaders’ part of its Magic Quadrant for Cloud Infrastructure as a Service.

It even became the target of a global major itself. Recognizing the depth of its relationships worldwide, Nippon Telegraph and Telephone bought Dimension Data in 2010.

The Innovation(s)

Dimension Data’s main innovation consists of Service as a Service. Yes, you read that correctly. The company must figure out how to integrate network, voice and data communications, data centers, contact centers, security, and Microsoft software – along with cloud and internet – for each of its clients. Its reach into 114 countries requires forming ongoing relationships with literally millions of companies in these jurisdictions. Most businesses work on an arms-length basis – the Coca-Cola Company can sell millions of cans of Coke without understanding each customer and Facebook can sell automated advertisements to millions of companies across borders because the company does not need to engage in a deep and serious long-term understanding of what the customer wants. Dimension Data, on the other hand, must reach deep into each client’s business – understanding their goals and psyche in order to put them within digital’s reach. Who would think IT and computer ‘geeks’ could value people as much as hardware?

Service as a Service (namely focusing on building long-term relationships with customers to adapt to their IT needs) represents an innovation for three reasons. First, the company acts as a ‘relationship surrogate’ – managing relationships with Microsoft and Cisco, by providing services and technical support for these global giants at the grass roots level. The company manages these relationships almost ‘by proxy.’ Second, Dimension Data partitions off specific relationships into subsidiaries – both by technology type and location. That means a Brazilian airline interested in talking to the company’s Brazilian cloud services person can make the right connection. Such divisions keep the company from becoming a monolithic bureaucracy. Third, by focusing on relationships, the company can branch out into any area or industry it wants. From networking to mobile telephony, the company can provide advice on almost any subject. By having strong relationships, the company can capitalize on its ‘relationship capital’ to cross-sell its 11 ‘solutions,’ 5 ‘services,’ and 40 ‘technologies.’ Close relationships also help the company market its services – as it often knows its clients needs before they do.

The Future

The company sits in an uncomfortable position – providing both a weakness and an opportunity. On the one hand, Dimension Data competes in the upper-income jurisdictions against cloud services providers like Amazon, Apple, IBM, Microsoft, and Google – just to name a few heavy-weights. Millions of small and medium-sized companies vie to advise companies on network integration and remote computing in the developed world. On the other hand, Dimension’s inroads into Sub-Saharan Africa make this company a bridge between the North and South. Internet penetration rates on much of the continent still remain too low (less than 10% of the population) to make Dimension’s services extremely profitable. The prospect of infrastructure, business, and other development leading to an internet revolution in Africa appear exceedingly dim. If the company could present a compelling strategy for cornering networking and cloud computing markets in Nigeria, Kenya, Ghana, and Tanzania at their next Investors Day, that would attract some attention!

Russia’s most promising innovative companies

Sector: Software

Sector: Software

Established: 2003, as spin-off from original company established in 1997

Origin: Moscow

Headquarters: Moscow

Revenue: $15.5 million

Employees: 130

Global presence: main company in Russia, with additional companies in Canada and Germany

In 2003, Kaspersky Anti-Viral software was already a household brand in many markets beyond Russia (now it is used by over 300 million users around the world), when the company found itself in an unusual business circumstance. The founders and owners decided to divorce, and in this case the word was not a metaphor. Evgeny and Natalya Kaspersky, a husband and wife and also the top managers of Kaspersky Lab, had to find a way to split their estate.

Natalya (who is now among the most successful Russian businesswomen and was ranked fifth in Forbes’ Richest Russian Women in 2013) opted for the smaller part of the business that was targeting the corporate market with a solution for Data Leak/Loss Prevention (DLP). These systems are designed to detect potential data breaches or data ex-filtration transmissions and prevent them by monitoring, detecting, and blocking sensitive data. In a sense, this is the ‘reverse’ task of the one traditionally solved by information security programs. Those were protecting personal or corporate systems from external threats – infiltration, viral attacks, etc. – while DLP systems look at the corporate networks (the product does not make sense for an individual) to find illegal actions by authorized users.

The company’s flagship product is called Infowatch Traffic Monitor and it permits control over all types of user actions within the network, from e-mail and on-line forum usage to printing out and copying of documents to data storage devices. Since 2012, the product has been on the Gartner Magic Quadrant, meaning it is recognized as one of the 12 top global solutions in its field.

The company is dominant on the Russian market with 39% of market share. The market in itself is dynamic enough to provide for double-digit sales growth (36% in 2013), yet the company actively seeks out opportunities for international expansion. It sees its core markets to be Europe, the Middle East, and, of course, the ex-USSR countries. Unlike many other Russian innovators, the company does not rely solely on organic growth; it has a story of successful acquisitions, which led to the formation of a holding in 2011. Besides the ‘original’ InfoWatch Ltd., which focuses on the DLP software, the Infowatch group includes German EgoSecure GmbH (end-point security software) and Canadian Appercut (business application source code analysis).

The

company also seeks to expand its markets down from the big enterprises

(its client list includes Gazprom, Lukoil, Transneft, VympelCom,

Sberbank, and Raiffeisen Bank, to name a few) to small and medium

businesses. Another prospective area of development is the mobile DLP –

increasingly important as corporate users frequently employ personal

mobile devices for business purposes. Thus, Gartner forecasts the global

market of DLP solutions to grow by 25% in 2014 to $830 million. The

Russian market demonstrates an even higher rate of growth, so the

dominant position that Infowatch has already managed to secure makes the

future of the company bright. In 2014, Infowatch was recognized as one

of the 20 most promising enterprise security companies in the world by CIO Review magazine.

Sector: ICT: audio forensics and voice biometrics

Sector: ICT: audio forensics and voice biometrics

Established: 1990

Origin: St. Petersburg

Headquarters: St. Petersburg

Revenue: $30 million

Employees: 350

Global presence: subsidiary office in the USA, partners in Belarus, Finland, and Germany. Sales in 74 countries

The Speech Technology Center is number one in Russia and one of the key global players in the audio forensics and voice biometrics market, those products that allow people to be recognized by their speech in real time. The bulk of the applications lie in the sphere of security, including the post-9/11 national anti-terrorism systems.

The company was founded in 1990 in St. Petersburg by a group of young researchers from the applied acoustics department of a state-owned telecommunications equipment producer. Their first office was just a typical two-room apartment shared with a fellow group of young businessmen. They managed to get the police interested in the new technology, and in 1993 they got a contract from the Ministry of Internal Affairs for the development of the ‘speech editor’ – a computer program which could process and analyze human speech. Software like that can be easily downloaded from the internet now, but at that time, real-time speech analysis posed many research and programming challenges. The product, called SIS, proved successful and was effectively used as the ‘core’ for creating numerous applications.

At the end of the 1990s, the company started exporting its product, presenting SoundCleaner Solution in Western Europe and the United States. This program used sophisticated sound processing to distinguish a signal – usually the human voice – from many noises, making it possible to understand a message from one person speaking amidst a very loud background. The excellent technical quality, combined with an attractive price, conquered the market; in 2001, the Madrid police ordered the system to process emergency calls.

Among the landmark achievements of Speech Technology Center was deciphering the recordings made by the crew of the Kursk submarine, which sank in a tragic accident in 2002. The tape recording spent nearly a year at sea in 100 meters of water and was assumed to have been destroyed. In 2004, the Speech Technology Center provided some of the key evidence in the case of a serial killer in Belgium, which had been under investigation for eight years.

In 2003, the company managed to attract investment from the European Bank of Reconstruction and Development, which provided resources for further expansion in the international markets (the company now officially sells and supports its products in 75 countries). A key achievement was the development of a language-agnostic system of identification through voice, which is in the core of the VoiceNetID range of products. In 2008, the company’s noise cleaning technology was recognized as the best in the world at the Audio Engineering Society convention in Denver (USA). In 2010, STC’s Smart Logger II (a system that manages call recording and monitoring for small offices and distributed contact centers) was named Communications Solutions Product of the Year by Technology Marketing Corp. Overall, the company is ranked second in the world for voice identification systems by the American SpeechTEK magazine.

Speech Pro USA, which operates in New York, is an established player on the American market. One of its most innovative – though very targeted – solutions is a miniature device which enables communication between NASCAR drivers and their coaches and teams. It eliminates the roaring of the engines, saving precious seconds of time – and also saving lives.

The new technological developments permit the company to start to target the end-consumer market. They have introduced the VoicePin app for mobile phones, which prevents anyone else from using your device. Innovations like these permit the company to grow its sales by 20% a year, with a target of making two-fifths of its revenue from exports. The global voice recognition systems market is expected to more than double in the next two years to over $2.5 billion in 2016. To capture a share of this growth, CST has just released it new recognition and synthesis version in English, the most popular language in the international software world.

Sector: Safety systems in the nuclear and gas industries

Sector: Safety systems in the nuclear and gas industries

Established: 1990

Origin: St. Petersburg

Headquarters: St. Petersburg

Revenue: N/A

Employees: 600

Global presence: subsidiary office in the US

Diakont specializes in television systems with a high resistance to radiation, creating products that are setting quality standards not only in Russia, but also in the US and other countries with developed nuclear energetics. General Electric, which is the largest American operator of nuclear power plants, buys up to half of its monitoring cameras from Diakont. The total number of installations in the US market is over 100 – an impressive figure in this very specialized field.

One of the founders of the company, Mikhail Fedoseevsky, acquired his advanced knowledge of the problems of electronic equipment radiation protection while working in a state military institution engaged in developing the Soviet response to Reagan’s Strategic Defense Initiative (aka ‘Star Wars’). During perestroika, he founded a company to design, manufacture, and market the radiation-resistant TV cameras. The first order came from the operator of the Soviet fleet of nuclear-powered Arctic icebreakers. The system permitted visual monitoring of the reactor, which radically decreased the cost of maintenance and repairs. Later versions of this product permitted remote control of the camera through a special manipulator capable of moving it to any part of the reactor.

In 1997, the first export contract followed, with ABB TRC from Sweden. The hard currency flow finally turned the innovative company into a fully profitable venture – prior to this, the founders had to engage in trading in consumer goods in order to keep afloat. In 2001, the company started selling in France, and a year later, it ventured into the US, the biggest potential market for its equipment in the world. There, Diakont managed to sell not only to GE, but also to its archrival Westinghouse, as well as to a subsidiary of French AREVA. Now, the company commands 60% of the US market for radiation-resistant cameras (and 90% of the Russian market).

Nevertheless, the company’s operations are limited by the narrowness of this niche market. The company produces systems in a total global market that only consists of dozens of installations a year. Finding another market that utilizes the same set of competencies is not an easy task. The company is currently investing in the development of complex steering systems – consisting of precise mechanics, electronic meters and processors, and analytical software – to replace the outdated hydraulic systems in cars, planes, and ships. The potential size of the new market is billions of dollars – and Diakont considers itself to be in the global top five for technology quality and market readiness. We will soon see if this estimate is correct.

Sector: Machine building, instrument engineering, and electrical engineering

Sector: Machine building, instrument engineering, and electrical engineering

Established: 1993

Origin: Belgorod

Headquarters: Belgorod

Revenue: N/A

Employees: N/A

Global presence: exports to Austria, Belgium, France, Germany, India, Italy, and the US

While the majority of innovative Russian companies are concentrated in or around Moscow and St. Petersburg, there are some important cases that prove that both genuine private enterprise and technological skill are in no way limited to these two cities.

Skif-M comes from the midsize city of Belgorod (population: 350,000) in the south of European Russia, some 700 kilometers from Moscow. The company specializes in cutting tools for metal and wood processing, such as drills, saws and replaceable blades. The company’s specialty is tools for those materials that are notoriously difficult to cut like tough stainless steels, aluminum alloy, titanium, and nickel.

The company was founded in 1993 in the research laboratory and experimental manufacturing unit of the Belgorod Mechanical Plant, which was founded in the Soviet era to produce aerospace industry tools. The company’s engineers managed to produce some of the designs and technologies that were rejected by plant management, and found their own clients among the leading domestic aircraft manufacturers, like MiG, VSMPO-AVISMA (the world’s biggest titanium company), and the Boeing plant in Russia’s Urals.

Now over 30% of the company’s output is exported to industrially developed countries like Austria, Belgium, France, Germany, Italy, the US, and also to India’s expanding automotive makers. Their competitive edge lies in high product customization – over 50% of the tools are made to customers’ unique specifications.

Skif-M tools are internationally recognized for their effectiveness in complex metal processing, which is based on two streams of research: the constantly improved geometry of their blades and successful experimentation with their coating, now employing nano-technological materials.

The company is not just involved in manufacturing. Much of the production is now performed by computer-controlled machines, which developed their own engineering center that is responsible for technological process designs and software development. Here lies the foundation for future strategic growth – building ‘turn-key’ solutions to the specifications of some of the world’s most demanding clients.

Head of the Digital Technologies at the SKOLKOVO Institute for Emerging Market Studies